How to get your free credit report online: A step-by-step guide

Getting your hands on a free copy of your credit report and checking it for errors is one of the easiest ways to help your financial health. Correcting even a small mistake can make a huge difference to your score. A higher score means lower interest rates, insurance quotes, and can even help you land some types of jobs. And it's never been easier to get a copy of your free credit report.

AnnualCreditReport.com is a government-approved site that enables most people to gain access to their reports within minutes. Under law, you have the right to obtain a free credit report from each of the three major credit bureaus once every twelve months. Courtney and I stagger our requests so that we are able to access a different bureau every four months.

Ralph writes:

I'd like to know how to get a free copy of my credit report from the agencies.

A recent federal law gives consumers access to their credit reports; however, it costs extra to obtain your credit score. Your credit score is not an actual component of your credit report.

The Fair Credit Reporting Act (FCRA) requires each of the nationwide consumer reporting companies — Equifax, Experian, and TransUnion — to provide you with a free copy of your credit report, at your request, once every 12 months.

There is never a need to go through any other agency to obtain your credit report. This is an official, government-approved site. If you'd like, you can obtain reports from all three credit reporting agencies at once. Or, you can stagger your requests, possibly requesting one report every four months from a different agency. There are three ways to obtain your credit report:

- Order it online at AnnualCreditReport.com.

- Call 1-877-322-8228.

- Complete the Annual Credit Report Request Form and mail it to: Annual Credit Report Request Service, P.O. Box 105281, Atlanta, GA 30348-5281.

You will need to provide some basic information, including your social security number, and you may need to provide some personal financial information. If you plan to check your report online, be wary of impostor sites. Be absolutely certain that you have reached AnnualCreditReport.com.

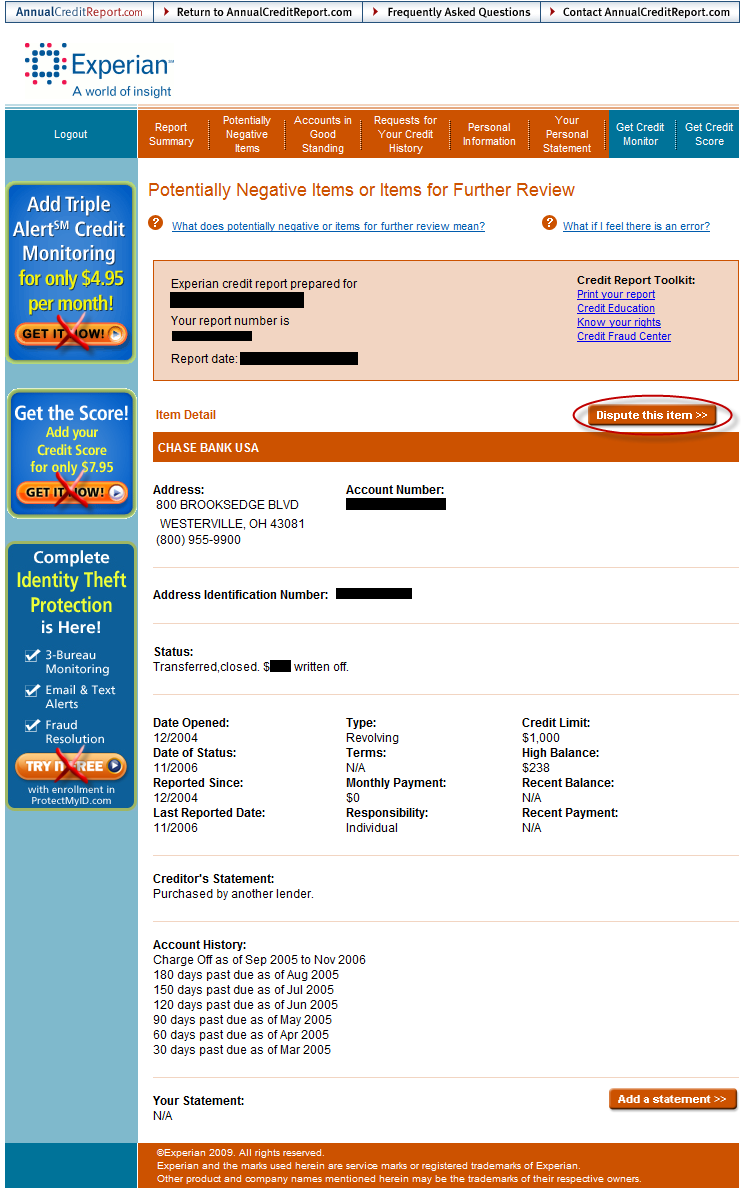

It's important to obtain a copy of your credit report at regular intervals. The credit reporting agencies are not infallible, and neither are your creditors. People make mistakes, and mistakes on your credit report can cost you money. If you suspect an error, read how to dispute credit report errors.

When you request your free credit report, you'll also be given a chance to purchase your credit score for about $8. Your credit score is a single number that serves as a snapshot for your overall creditworthiness, a sort of summary of your entire credit report. To learn how your credit score is computed, read my anatomy of a credit score.

How to Obtain Your Free Credit Report

I don't think people realize just how simple it can be to check your report! Below, I've taken step-by-step screen shots of each leg of the process:

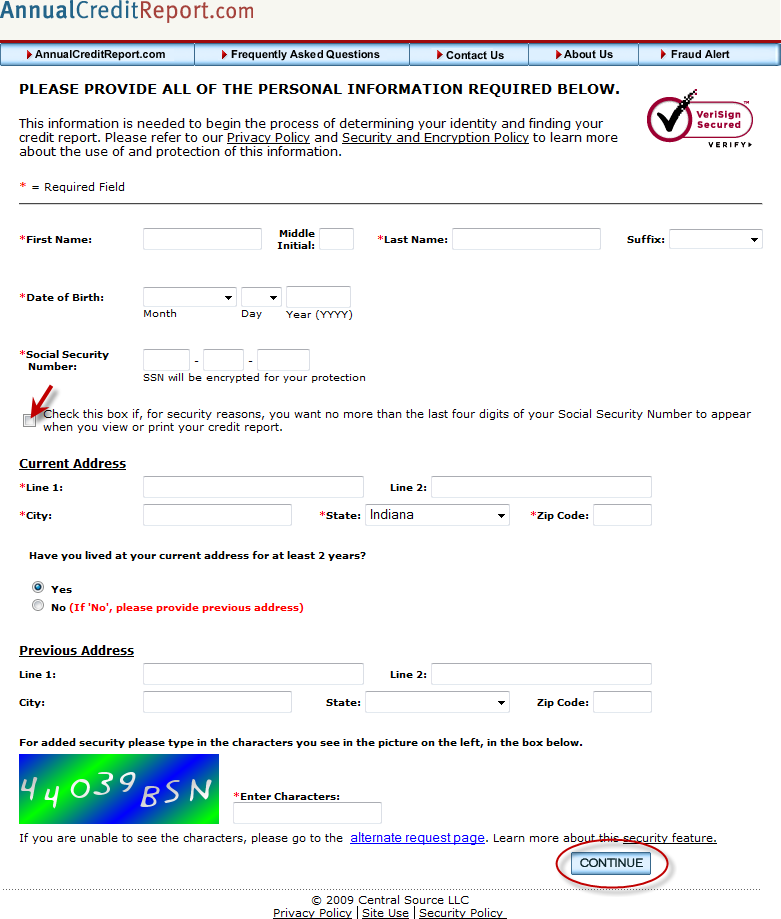

- Next, enter the required information (marked with a red *).

- I recommend checking the box (I've highlighted with the red arrow) to hide your social security number should you print out the report.

- Enter in the security code and select “Continue”.

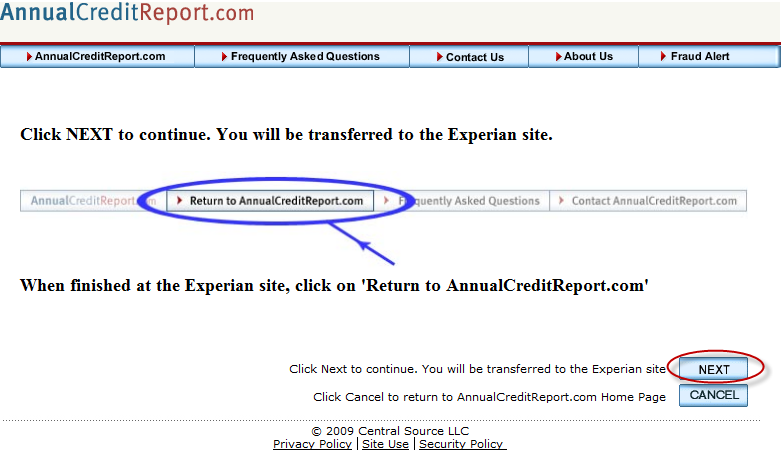

- On this page you can select the bureau (or bureaus) you'd like to get your credit report from.

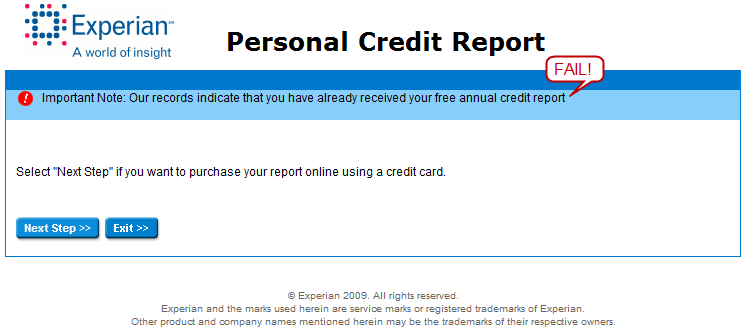

- You can view all at once, but you'll have to wait another full 12 months before re-visiting the same bureau. (In other words, if you pull all three at the same time, you can't check any of them for free for an entire year.)

- Courtney and I stagger our request and only pull one every four months.

- Click “Next”.

- This screen is just a confirmation that you'll be visiting the specific site of the bureau you selected.

- Click “Next”.

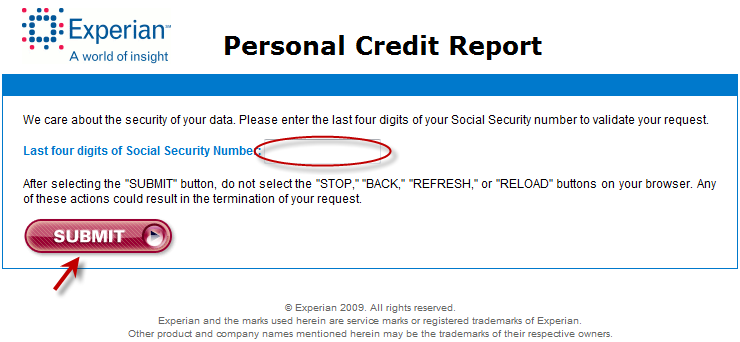

- You are now asked to verify your identity on the specific site of the bureau.

- This is Experian, although TransUnion and Equifax have similar confirmation screens.

- Enter your information and press the red “SUBMIT”.

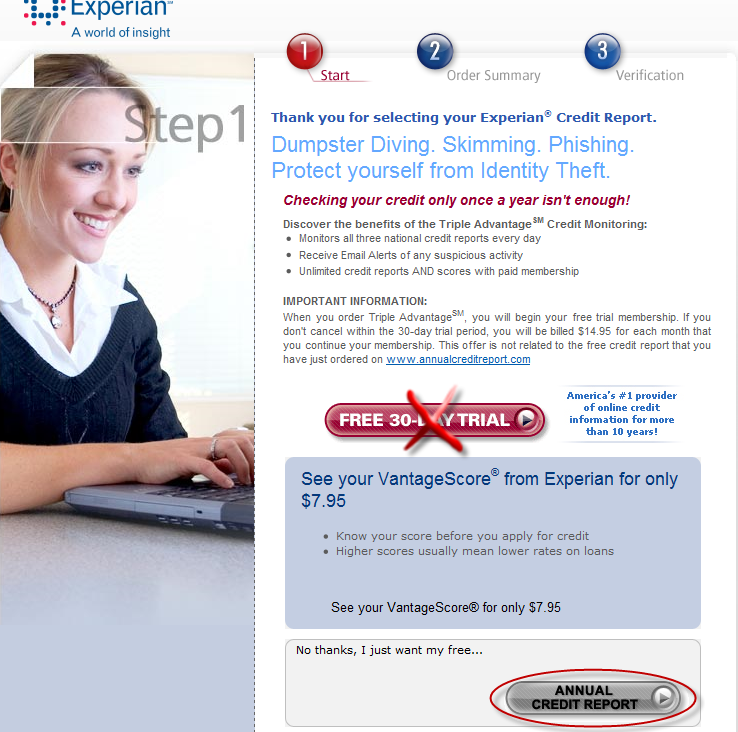

- Experian would now like to make a quick buck.

- Avoid the upsell, and click “Annual Credit Report” highlighted below.

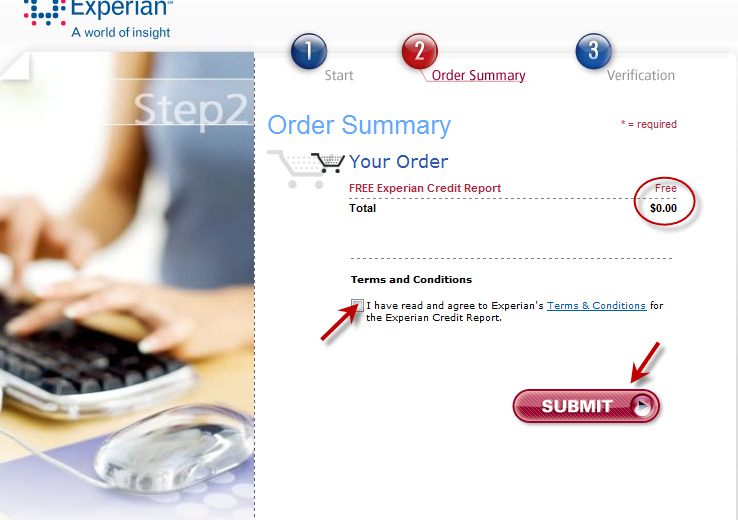

- Next is the Order Summary screen.

- Verify the amount is $0.00 (Free).

- Check the Terms & Conditions box. (If your name is J.D., you'll want to read the whole damn thing before checking the box.)

- Click the red “SUBMIT” button.

- Lastly, you have one more confirmation screen before gaining access to the report.

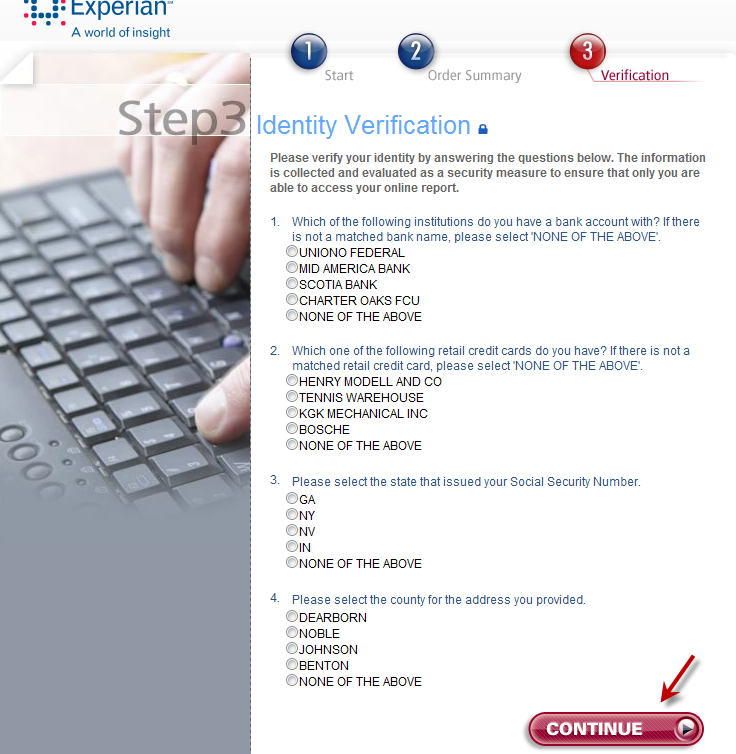

- Experian asks you four security questions regarding information on the file.

- Answer the questions (some may very well be “NONE OF THE ABOVE”).

- Click the red “CONTINUE” button.

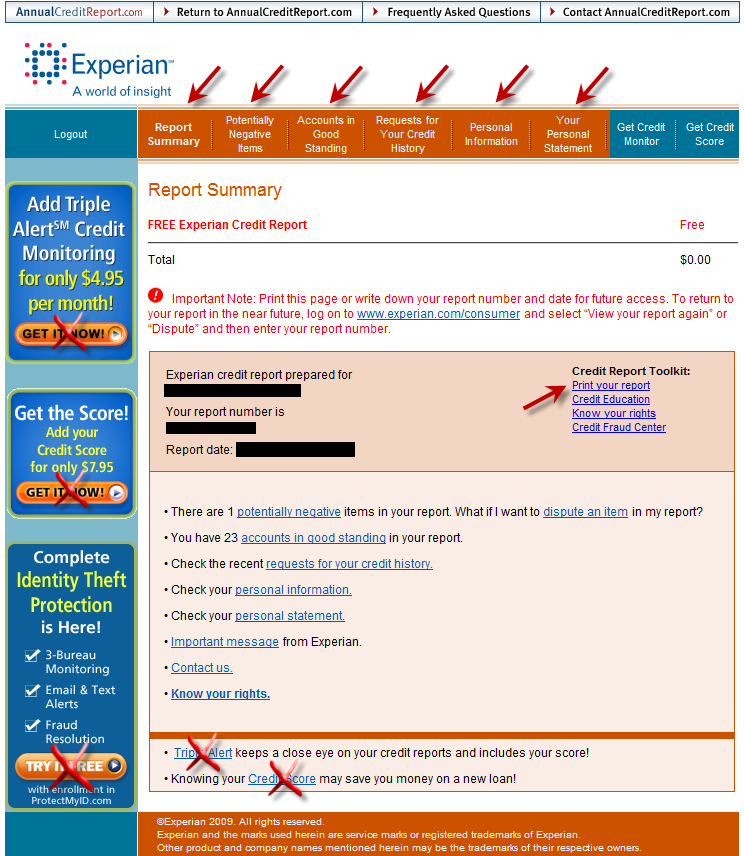

- Now you have access to your credit report!

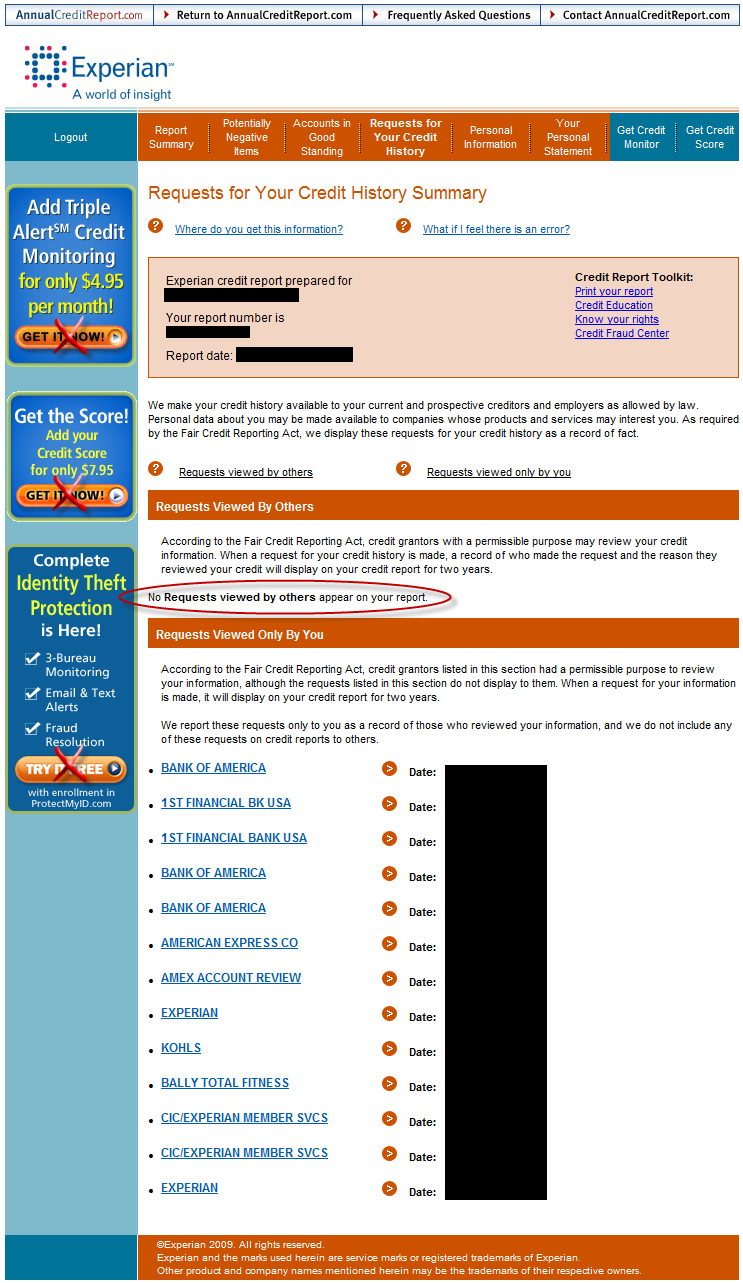

- Look over the Summary, Negative Items, Accounts in Good Standing, Requests, Personal Information, and Personal Statement tabs at the top.

- Notice the “print your report” link I've highlighted in case you want to retain a copy.

- As always, avoid the upsells to keep your access free!

In the rare case you are denied access…

If for one reason or another you are unable to obtain online access, you still have options for getting your free reports. You can:

- Call 1-877-322-8228 to obtain a copy by phone; or

- Complete the Annual Credit Report Request Form and mail it to: Annual Credit Report Request Service, P.O. Box 105281, Atlanta, GA 30348-5281.

FreeCreditReport.com vs. AnnualCreditReport.com

Mark Frauenfelder (founder of the awesome Boing Boing) has a piece at PC.com that asks: When is a free credit report not a free credit report? The answer, of course, is: When it comes from FreeCreditReport.com.

FreeCreditReport.com, which has raised the ire of many, does allow people to look at their credit reports free for seven days, but then automatically enrolls users into a $15/month credit monitoring service. This last fact is a problem. Frauenfelder writes:

I clicked on the large bright orange button that said “Get your Free Credit Report & Score!” and was presented with a form. I filled it out. I hesitated for a second when the site asked for my credit card number, which it stated was “required to establish your account,” but the site assured me that my “credit card will not be charged during the free trial period.” Having done this before (or so I thought), I went ahead and entered the information. A shopping cart receipt indicated that the total was $0.00.

I got my credit report, looked it over, and forgot about it. A week later I was looking at my checking account register online and I noticed a $14.95 charge from a company called CIC*Triple Advantage. I didn't recall buying anything from a company with that name, so I entered “CIC*Triple Advantage” into Google. The search results made my eyes bug out of my head. This was the name of the billing entity for freecreditreport.com. The thousands of search results were full of words like “deceptive practices,” “scam,” “ripoff,” “unauthorized billing!” and “beware!” In fact, all the top results were either from people complaining that they'd been conned into signing up for a $14.95 monthly credit monitoring service without their permission, or they were about how to cancel the service.

Frauenfelder admits that it's his fault for being duped, but still thinks FreeCreditReport.com is slimy. Read the rest of his story for other problems he has with the service.

Finally, on a lighter note, a post in the GRS forums pointed to this spoof commercial highlighting the problems with FreeCreditReport.com.

Your Credit Report Card

Credit.comlaunched a free new online financial tool called Credit Report Card. This tool is designed to provide users with a quick snapshot of their credit reports. According to the site's FAQ, “it breaks down your credit report into five simple-to-understand categories and gives you a letter grade for each one.”

Here are some things to know about Credit Report Card:

- It's absolutely free.

- You can request a new report card every thirty days.

- It draws its data from the TransUnion credit bureau.

- Its data comes via a “soft pull” of your credit, so using it will not affect your credit score.

Curious, I signed up for Credit Report Card myself. Some GRS readers will be wary because the sign-up process requires that you submit your Social Security Number (which is needed to pull your credit report) and asks a couple of broad but personal questions. I felt comfortable with this, though, and created an account.

My overall credit “grade” is an A. I scored high in the areas where I knew my report was strong, and I scored a little lower in the areas where I knew it was weaker. (Though I do have a personal credit card now, I try to avoid credit when possible, so I don't have as broad an “account mix” as I could.)

The bottom of the report contained a summary of the statistics used to produce the Credit Report Card. You can see that I spend about $1000 a month on my credit card, which I diligently pay in full. (This earns me about $10 a month because it's a 1% cash back card.)

Each section of the Credit Report Card also contains a detailed explanation of how your grade was derived. These sections contain a couple of paragraphs each explaining how credit scores work and recommending actions you can take to improve your credit.

The Credit Report Card isn't earth-shattering. It's not a tool that's going to revolutionize the way you deal with money. It is, however, a useful way to monitor your progress. I've added the site to my bookmarks, and I plan to check in every month or two when I'm doing my personal finances.

Get Your Free Credit Report

So what are you waiting for? If you've put this off in the past, schedule a time to get your free copy and review it for errors! Your credit score and your wallet will thank you.

Become A Money Boss And Join 15,000 Others

Subscribe to the GRS Insider (FREE) and we’ll give you a copy of the Money Boss Manifesto (also FREE)