How and why you should start an emergency fund

Most personal finance experts agree: The first thing you should do — after meeting basic needs — is to establish an emergency fund.

Life is full of unexpected surprises, many of which cost money — a thief smashes the windshield of your car, your son gets sick, your water heater overflows. When people live paycheck to paycheck without any savings, they’re at the mercy of these small crises. Sometimes a tiny problem becomes a huge one because the victim wasn’t prepared for possible trouble.

That’s where the emergency fund comes in.

What Is an Emergency Fund?

An emergency fund — or “rainy-day account” or “safe and sound money” or whatever you’d like to call it — is a chunk of change set aside specifically for the unexpected things life throws your way. It’s not to be used to buy a new car. It’s not to be used for a vacation to Paris. It’s not to be used to remodel your bathroom. It’s for use only in case of emergency: a tree falls on your house, your youngest daughter breaks her arm, you lose your job.

I have a couple of friends who believe emergency funds are unnecessary. They’re wrong. Maybe emergency funds are unnecessary if you’re rich. But these friends aren’t rich. For most people, emergency funds are a form of self-insurance. They’re a proactive way of protecting you and your family from random crappy events.

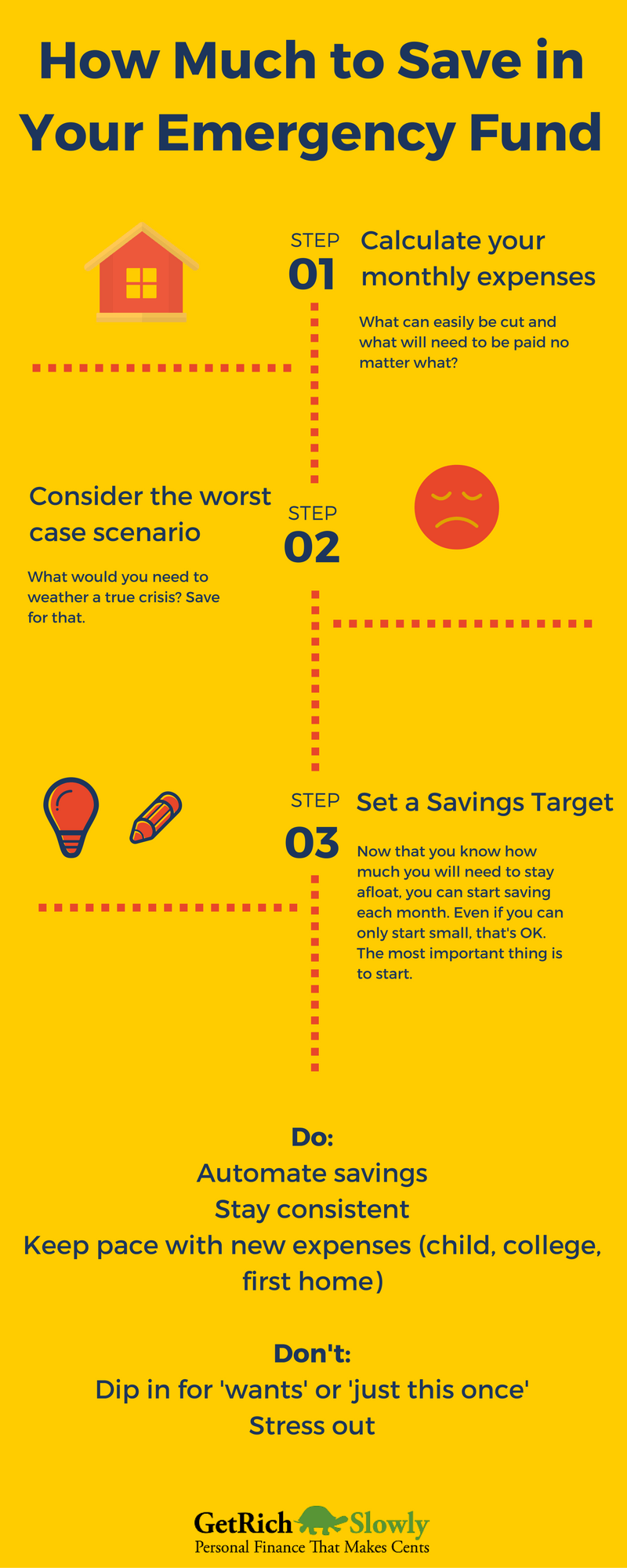

How Much to Save in an Emergency Fund

Though personal finance experts agree emergency funds are necessary, there’s no consensus on how much is enough. Here are just a few recommendations:

Though personal finance experts agree emergency funds are necessary, there’s no consensus on how much is enough. Here are just a few recommendations:

- In The Wealthy Barber, David Chilton argues that it’s best to have adequate insurance to cover the big emergencies, and to set aside between $2000 and $3000 to cover small crises and the things that insurance won’t cover.

- In The Six-Day Financial Makeover, Robert Pagliarini writes: “Your emergency reserve is your financial cushion in case something goes wrong and you lose your job or you need access to money quickly. Your emergency reserve should consist of at least three months’ worth of cash. Once you’ve saved enough for the cushion, you can [move on] to other goals.”

- In You Don’t Have to Be Rich, Jean Chatzky recommends three to six months of living expenses.

- In Your Money or Your Life, Joe Dominguez and Vicki Robin recommend six months of living expenses — but only once you’ve achieved financial independence. Before that, they want you to put your money toward debt reduction and wealth building.

- In The Total Money Makeover, Dave Ramsey recommends a two-stage approach. First, before anything else, set aside $1000 to cover emergencies. Then, after you get out of debt, boost you emergency fund to cover 3-6 months of living expenses.

My own advice is to do what works for you.

Start small. If you don’t currently have a rainy-day fund, then anything is better than nothing. Set aside $500. Or $100. Or $20. Over time, work to build this buffer until you have $1000 or $5000 on hand for catastrophe. Ultimately, you’ll sleep more soundly if you do have six to twelve months of living expenses in the bank. It’s a comfort to know that if you lose your job, you won’t lose your home right away.

How to Start an Emergency Fund

Starting an emergency fund is totally non-difficult. Anyone can do it. Here’s how:

- Pick a bank. I’m a fan of local credit unions and community banks, but I also like high-yield savings accounts at online banks. (My emergency fund is at Capital One 360, although there are plenty of other options.)

- Build a buffer. If you’re still in debt, it’s probably best not to stick a lot in savings. You should set aside $500 or $1000 to deal with annoying emergencies like a car that breaks down, but the rest of your money should be thrown at your debt.

- Resist temptation. When you have a big chunk of change sitting in the bank unused, it can be tempting to use it for other things. Resist the urge. Use your emergency fund only for emergencies, otherwise you defeat the purpose.

- Save more. As your debt dwindles, and as you get better control of your finances, build your emergency fund. Pick a number that helps you sleep at night. For me, that number was $10,000. That seemed like a lot of money to me (and still does!), and if anything disastrous happened, it would help me survive for a long time.

Finally, it’s wise to keep your emergency money someplace that’s not too easy to access. (Ignore this piece of advice if you know you’re disciplined enough not to use the money for other purposes.)

You might, for example, open an account at a bank across town. Or deposit the money with an internet bank. Or put the money into a certificate of deposit. Don’t carry a debit card tied to your emergency fund. You’ll still have access to the cash when you need it, but you’ll be forced to consider your actions before making a withdrawal.

When Is It Okay to Use Your Emergency Fund?

But what is an emergency? This is an interesting question, and one I’ve thought about a lot lately. How do you decide what is and what is not an emergency?

Sometimes the answers are easy, of course. A vacation to Florida is not an emergency and should not be funded from your emergency fund. New boots are not an emergency, and neither is a new videogame console. On the other hand, if your only car is totaled, buying new transportation is an emergency. Or if your son breaks his leg, his medical expenses are an emergency.

But what about all the stuff in between? What if your computer dies? Is that an emergency? Or should you just go to the internet cafe? What if the garage roof starts to leak? What if you have an unexpected dental bill?

Ultimately, I think the key is to decide for yourself what you emergency fund can be used for and what it can’t. But once you make that decision, stick to it.

Final Thoughts

From experience, I know that it can sometimes be painful to see a large pool of money sitting unused for months (or years) on end. But also from experience, I know that when a natural disaster strikes (or any other kind of disaster, for that matter), an emergency fund goes a long way to preventing financial disaster as well.

Studies show that those without emergency savings are more likely to accumulate debt. Your emergency fund acts as self-insurance, cushioning you from small disasters. If you have a cash cushion, your financial plans can’t be derailed by a single unexpected event — unless it’s huge.

How much do you keep in your emergency fund? How did you choose this amount?

[photo by Incase]

Become A Money Boss And Join 15,000 Others

Subscribe to the GRS Insider (FREE) and we’ll give you a copy of the Money Boss Manifesto (also FREE)